The highlight of the month has been my immersion into artificial intelligence (AI). I’ve been working with different image-generation platforms and have been amazed with what is possible.

Just before writing this article, I created the image above with a wizard and his money tree, growing gold. It was created using Microsoft Designer (MSFT), taking only a few seconds.

AI aside, let’s take a look at how my dividend payments performed through May.

Table of Contents

Dividend Summary

I earned income from seven companies; four Canadian and three US.

CAD Dividends

| Company | CAD Payments ($) |

|---|---|

| RioCan Real Estate Investment Trust (REI.UN) | 23.49 |

| Chartwell Retirement Residence (CSH.UN) | 5.10 |

| Metro Inc. (MRU) | 6.05 |

| A&W Revenue Royalties Income Fund (AW.UN) | 6.40 |

USD Dividends

| Company | USD Payments ($) | Div Change (%) |

|---|---|---|

| AbbVie Inc. (ABBV) | 66.60 | |

| Apple Inc. (AAPL) | 3.60 | 4.35 |

| Walmart Inc. (WMT) | 7.27 | 1.79 |

I earned a record $118.51 in currency-neutral income in May, as a combination of C$41.04 and U$77.47. This represents a 14.71% YOY grow rate over May 2022.

It’s just a slight incline, but every bit counts:

Year To Date Progress

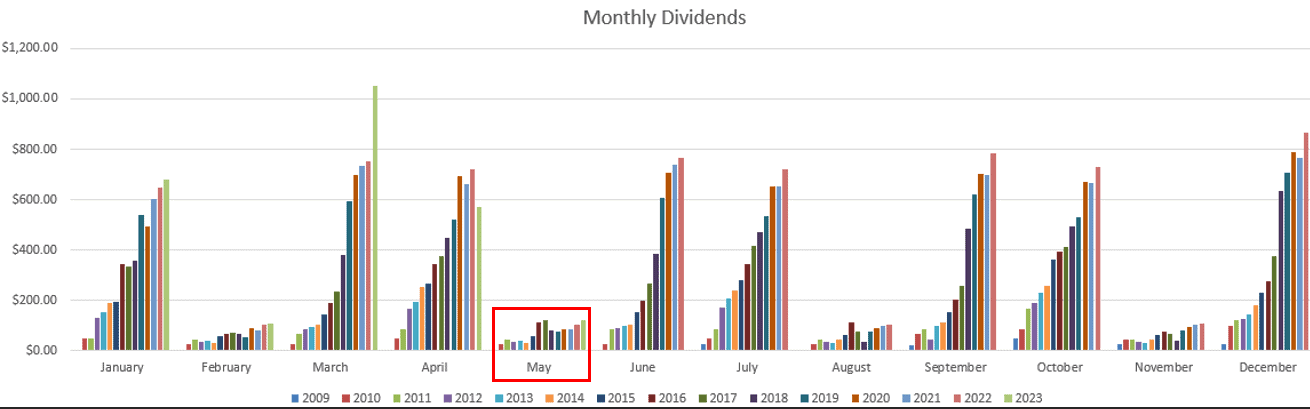

I’ve crossed the $2.5k mark over the course of the first five months:

| Month | Dividends ($) |

|---|---|

| January | 680.90 |

| February | 107.14 |

| March | 1,050.94 |

| April | 572.74 |

| May | 118.51 |

| Total | 2,530.23 |

This represents a ~$500 per month rate of passive dividend income, and that’s with two of my lowest months of the year included—February and May. June is likely to bring a sizeable total and swing the dividends-per-month total considerably higher.

Market Activity and Cash

Inflation remains above the Bank of Canada’s (BoC) targets. My personal belief is that there are simply too many inputs to think that increasing interest rates will be sufficient to tame inflation.

How can a 0.25% increase in interest rates in Canada truly offset a protracted war in Europe, along with all other global uncertainties? The BoC has a mandate and will do what it can, but there are many other factors at play which are increasing prices at the grocery store.

The other thing to consider is that the impact of increased rates will always take months or even years to see represented in headline CPI data. Someone who locked in a five-year mortgage term two years ago may only feel the pinch in three years. So, this takes time to shake out.

In the meantime, increasing interest rates and thus the cost of borrowing is itself a form of inflation.

How to balance it all?

Conclusion

My path forward remains the same. I’ll continue investing in high quality dividend paying companies and letting them do the heavy lifting. I reinvest selectively and allow compounding to work its magic.

Keep to your strategy and don’t sweat the market gyrations. If things swing lower, take advantage.

And most of all, enjoy the warmer weather while it’s here.

Thank you for reading. Full Disclosure: Long REI-UN, CSH-UN, MRU, AW-UN, ABBV, AAPL, WMT, MSFT