The key to successful investing is ensuring the money you have set aside is working hard for you. Whether you’re trying to buy low to sell high or whether you have adopted a cash flow driven strategy, the goal is to wind up with more money than you had at the outset. Foregoing consumption today for greater consumption in the future is the name of the game. One of my favourite metrics for assessing how effective I am investing is to review dividend yield on cost.

As a dividend growth investor, I place the greatest emphasis on how effectively my invested dollars are providing, and growing, regular dividend payments. The overall market value of my portfolio is far less concerning to me than how much money is being churned off in tangible cash flow. You can spend cash flow, while net worth is more difficult to access, particularly if locked up in illiquid assets.

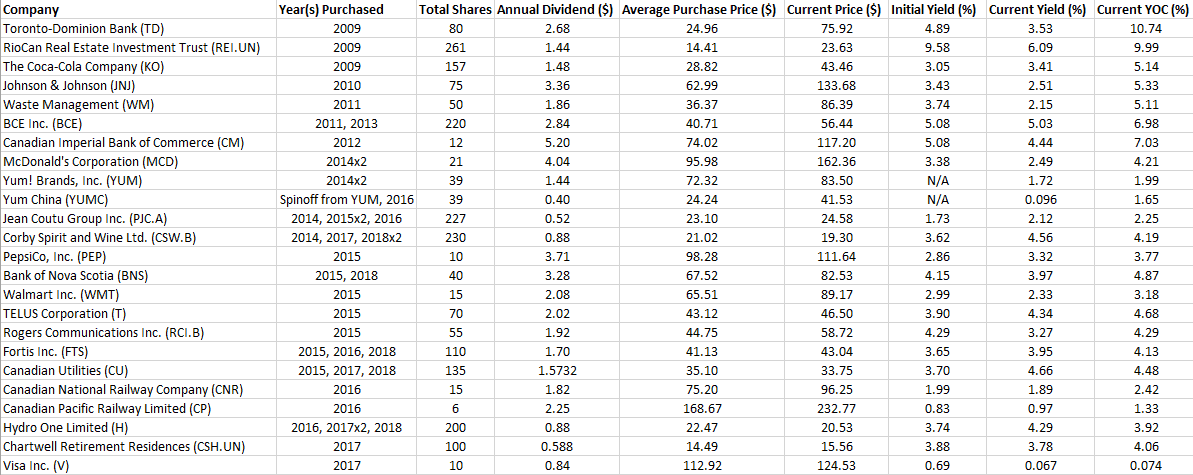

When I began my dividend growth investing journey back in 2009, I started off with an initial purchase of 40 shares (split-adjusted, I now own 80 shares) of Toronto-Dominion Bank (TD). I recently chronicled how my dividend yield on cost yield on cost has since doubled with TD. Following up on that theme which generated plenty of positive discourse, I will in this article take a holistic view of my overall portfolio to determine how well my dividend growth has been increasing over the years.

Table of Contents

Dividend Yield on Cost Spreadsheet

* Every effort was made to ensure the accuracy of this data. Annual dividends used are current as of my latest review. Please refer to company websites to ensure absolute accuracy.

* Every effort was made to ensure the accuracy of this data. Annual dividends used are current as of my latest review. Please refer to company websites to ensure absolute accuracy.

** Figures are in CAD for Canadian companies. Figures are in USD for U.S. companies.

*** Current price is based at the time of writing on Sunday, March 18, 2018.

**** For YUM and YUMC, I have decided against providing an initial yield given the spinoff.

Glossary of Columns

Year(s) Purchased: In some cases, I have purchased a company in multiple tranches. In this column I list the years I made my buys. While some companies (KO, BCE, etc.) have been DRiPed on occasions, I do not outline the dates of these passive reinvestments.

Annual Dividend: The projected annual dividend payment when monthly or quarterly payments are combined.

Average Price Paid: The average weighted purchase price. Relevant in cases where I have made multiple purchases of a company over the years.

Initial Yield: The yield I was earning on the occasions I bought the companies. In cases where there are multiple purchases, I will simply use the average purchase price to approximate an overall initial yield rather than showing multiple values which will only obfuscate what the chart is intending to show.

Current Yield: The current yield someone would receive if they made a purchase at prevailing prices.

Current YOC: My personal dividend yield on cost when factoring in my average purchase prices with the annual dividend as it currently stands..

Observations

The real benefits from dividend growth investing take time to materialize. With even a cursory glance at the chart, it is easily recognizable that the biggest gains in yield on cost tend to be weighted toward those positions I have held the longest.

Of the 24 companies listed, 22 have provided dividend increases over the years. None of the companies have cut their payments even a single time. RCI.B has maintained its dividend ever since I originally purchased it and YUMC only initiated a dividend payment last year and hasn’t had it for a full year on which basis I will eventually judge it.

The only dividend paying company I have owned which I eventually sold was Cedar Realty Trust, Inc. (CDR). At the time, it was known as Cedar Shopping Centers. I owned the company between 2010 and 2013 during which time its dividend had been sliced by 44%. I was then happy to eventually sell the position at a slight profit. It is the sole dividend cut I have been the recipient of and even then I was fortunate to realize a gain on the position.

Dividend Growth Investing Is Durable

The dividend growth investing strategy has proven incredibly stable over the years. Despite my portfolio’s inception in the midst of a financial crisis, the quality of the companies has shone through. I have come to trust the income produced over the years.

Also noteworthy when reviewing the years in which I made my purchases, I transitioned to a slightly more active style around 2014. Prior to that time I was paying commissions of around $30 per trade. Since then, I have been paying just under $10. At $30 I was comfortable with purchases of around $3,000 as this would mean a 1% commission. Likewise, on a $10 commission I now pay 1% on $1,000 purchases. This means I don’t need to wait as long before making buys and thus reap the dividends in the interim where otherwise I might miss them while building up an investable sum.

Initial Yield vs. Current Yield vs. Yield on Cost

One of the most common questions I receive is how to get a high dividend yield. There are basically two methods:

1) Purchase a high-yielding company in order to get a high dividend yield from the start.

2) Buy a low-to-moderate yielder and be patient.

The profile dividend-paying companies is such that high yielders (i.e., over 7%) tend not to grow their dividends by much. For the most part, these companies pay a high percentage of their earnings in the form of a dividend, retaining very little to continue growing the company. As a result, the investor receives a sizeable payout with less opportunity for growth.

Further, these high yielding companies have a nasty habit in many cases of cutting their dividends. With a high payout ratio, there isn’t much on-hand to weather storms. When a company faces rocky times and doesn’t have financial flexibility, the dividend can oft come under fire.

With the security of your financial independence at stake, taking such risks isn’t worthwhile. Stick to best-of-breed companies that can grow their dividends consistently.

Yield on Cost Takes Time

It is possible to build up to a sizeable yield on cost if an investor can be patient for a few years. TD, for example, is widely regarded as one of the best banks in North America. I currently receive a yield on cost of over 10% even though I initially was only getting paid 4.89%. If I had sat on the sidelines waiting for TD to offer me a starting yield over 10%, I’d still be sitting with my cash in hand. At no point over the period of my investing period (beginning May 2009) did TD offer a yield this high. After buying TD, all I had to do was sit back and receive the income over time as my yield on cost continued to grow.

With JNJ, I picked up my shares during the midst of concerns over product recalls. The price had been stagnating as investors called for change at the management level. As a result, the dividend yield had entered into tempting territory, sitting at 3.43%. At that point I decided JNJ was well worth the risks and made my purchase. Since then the shares have been rising steadily and although my current yield is only 2.51%, I enjoy a solid yield on cost of 5.33%.

Trading Ranges

Many companies trade over the years in a similar range. Using yield as a valuation metric, many companies will seem to pay a similar current yield as the years pass. For BCE I have an initial yield of 5.08%, it offers a current yield of 5.03%, and my yield on cost is 6.98%. What this means is that the share price has actually risen roughly in tandem with the increase in dividend payment. Getting that double dipping benefit of yield and capital both increasing is one of the secret ingredients for dividend growth investors.

Paper Gains/Losses

When I view my holdings, I only really become interested when the stock price has pulled back. I tend to largely ignore the stocks that have increased and pay close attention to those experiencing declines. When a stock decreases in price but maintains a steady dividend payment amount, that means an investor is offered a higher starting dividend yield. That’s the sort of thing that excites me.

Still, if ever there was a free lunch in dividend growth investing, the capital appreciation that goes along with a rising dividend would be it. While the rising cash flow is my goal, seeing my portfolio’s bottom line swell at the same time is a corollary benefit. The downside to your stocks increasing in value is that buying more will cost more, with a lower starting yield.

Conclusion

What I hope I have been able to demonstrate with this review of my portfolio is that while dividend growth investing takes time to reach a critical mass of income and the benefits do take years to fully realize, the reward can be well worth the wait. It is a strategy with concrete benefits for the patient investor who reinvests dividends earned and avoids the manic behaviour of rampant buying and selling.

With dividend growth investing, time is the investor’s greatest ally. The key is to focus on high quality companies with a proven track record of delivering dividend increases to their shareholders. With each dividend increase and each payment received, the overall portfolio strengthens.

As a result of focusing on quality, I do not worry when the market has a correction. In fact, the bigger the dip, the higher my level of interest in finding bargains. While the short-term vicissitudes of the market are based purely on investor sentiment, dividends are doled out based on actual business prospects. For my money, I’d rather trust my fortunes to the latter.

I hope you enjoyed this deeper dive into my portfolio and the benefits of dividend growth investing. I look forward to discussing the strategy further with each of you.

Thank you for reading.

Full disclosure: Long TD, REI.UN, KO, JNJ, WM, BCE, CM, MCD, YUM, YUMC, PJC.A, CSW.B, PEP, BNS, WMT, T, RCI.B, FTS, CU, CNR, CP, H, CSH.UN, V

Pictures courtesy of pixabay.com

Totally agree with your post, but though I watch YOU, it’s the income generation I concentrate on. How much, how it is growing and by how much compared to previous years.

We slowly cut our holdings and now only have 12 stocks in all our accounts. The concentrated portfolio is showing better growth than when we had 25. It’s only been a few years but I feel confident it will continue to grow.

Hi Cannew,

Yeah, I really view YOC as a metric to assess the efficiency of dollars invested. As you note, the important thing is to have a sustainable, growing income YOY as that is what drive capital appreciation as well.

It sounds like we’ve both identified the issue with having too many positions. I have committed recently to not opening new Positions (I don’t count my recent purchase of MRU as PJC.A merged with them). Instead, I’m doubling down on those companies already existing in my portfolio.

I appreciate the comments.

Take care,

Ryan

Get Rich Brothers, thank you for your blog post.Really thank you! Awesome.

Good afternoon,

I’m glad you enjoyed the article.

Take care,

Ryan